Payroll Tax 101 for the Business Owner

Like any good business owner in the U.S., you’ve been paying employees on time, and you’ve been withholding federal income taxes and Social Security/Medicare taxes. But your responsibility doesn’t end there — now you must report the amounts that you have been withholding and pay those amounts, including your business’s required payments,to the IRS.

The 941 Payroll form is an important quarterly payroll tax form for every employer, and it’s due four times a year. This form is due at the end of April, July, October, and January.

What Is the Form 941?

Payroll 941 is the form used by employers to report withholding amounts for federal income taxes andFICA taxes (Social Security and Medicare), employer payments for these withholding amounts, and any amounts due to the IRS.

Form 941 includes the following quarterly reports and calculations:

- Reports of amounts withheld frompaychecks for federal income taxes andFICA.

- Calculation of amounts due from taxablesocial security wages and Medicare wages for both the employer and the employees.

- Adjustments for sick pay and tips.

- Calculation of amount due in payment by the employer.

- Amounts already paid by the employer, on either a monthly or bi-weekly basis, depending on the total number of employees and the size of the payroll.

- Any overpayment or underpayment.

How Do I Complete and Submit the 941 Payroll form?

The form requires a calculation of the total taxes and the total deposits made during the period. The difference between the total taxes due and the total deposits is the amount still owed that must be paid.

Form 941 may be submitted electronically using FederalE-file. You can E-file Form 941 and pay any balance due electronically by using tax preparation software or by consulting with a tax professional.

How Do I Pay Taxes with Form 941?

In the event that you’ve paid the total amount of your payroll taxes during the months covered by this form, you’ll see “$0” due. But if you owe taxes, you cannot wait until you file Payroll Form 941 and pay all taxes for the quarter at that time. You must make either monthly or bi-weekly deposits, depending on the amount owed.

If you are required to make deposits, you may have a small balance due. Make that deposit electronically using the IRS EFTPS system. This is important: don’t pay your payroll tax deposits with your Form 941. The IRS clearly states: “If you’re required to make deposits and instead pay the taxes with Form 941, you may be subject to a penalty.”

What If I Made a Mistake in Completing Form 941?

It happens. The most common type of mistake made when completing the 941 Payroll form is entering the wrong amount in a box.

Errors in these amounts can lead to over-reporting which will result in paying too much, or under-reporting and paying not enough. You can opt to make an adjustment if you under-reported or if you both under-reported and over-reported. You can also file a claim if you just over-reported. However, you cannot make an adjustment and a claim on the same form. You must use separate 941X forms.

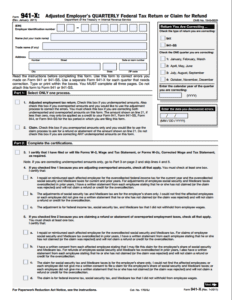

What is a 941X Form?

The IRS requires businesses to report Form 941 corrections on Form 941X, Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund. Form 941X is a form that correlates line-by-line to Form 941. Form 941X has five sections, which require you among other things to declare whether it’s an adjustment or a claim as well provide a detailed explanation of why you’re making the corrections.

You can only use the form for one quarter. If you’re reporting errors for more than one quarter, you must use a separate form for each. The process differs slightly if you file less than 90 days from the expiration of the period of limitations on corrections for Form 941 or more than 90 days from this date. The instructions included with the form explain what you must do in each circumstance. If your error affected employee withholding, you must obtain a written consent from each affected employee. You’ll have to certify this statement:

“I have a written statement from each employee stating that he or she has not claimed (or the claim was rejected) and will not claim a refund or credit for the over-collection.”

If you cannot get written consent from each employee, you can only make Form 941 corrections in the employer portion.

Payroll taxes can be confusing to both small and large business owners alike. If you have any questions about complying with the IRS’ rules, contact us for a free, no-obligation consultation.